A Brief Guide to SFDR Reporting and Compliance

When the European Union’s Sustainable Finance Disclosure Regulation (SFDR) came into force in March 2021, it signalled to the world that the EU was ready to take a global lead…

When the European Union’s Sustainable Finance Disclosure Regulation (SFDR) came into force in March 2021, it signalled to the world that the EU was ready to take a global lead on ESG reporting and sustainable finance.

The move impacted all financial market participants and financial advisors based within the EU. Along with the European Green Deal (which aims to see the bloc carbon neutral by 2050), and the EU’s “green taxonomy” (an industry-based classification system of what can and cannot be marketed as a sustainable product), a potent mix of regulatory mechanisms is set to usher Europe towards an economy in line with the Paris Agreement and the United Nations Sustainable Development Goals (SDGs).

Things are messier in North America. While Canada has opted for mandatory climate disclosures for Crown corporations starting in 2024, its powerful southern neighbour has shown a more chaotic approach to ESG. On the one hand, the US Securities and Exchange Commission proposed compulsory climate reporting for publicly listed US companies, yet the Supreme Court also ruled against the Environmental Protection Agency’s powers to curb greenhouse gas emissions.

Europe’s proactive stance could provide guidance or “lessons learned” for North American responses to the inevitable mainstreaming of ESG. Indeed, SFDR should matter to anyone interested in building the post-pandemic “economy 2.0.”

Update as of December 4th, 2023: The European Supervisory Authorities (ESAs) have recently published a Final Report that outlines proposed changes to the principal adverse impact (PAI) and financial product disclosure regulations under SFDR. These proposed modifications include improvements to sustainability disclosures in the financial sector, the introduction of new social indicators, and a streamlined approach to disclosing PAI associated with investment decisions pertaining to environmental and societal impacts. You can find the comprehensive Final Report by clicking on the following link: Final Report SFDR Amendments.

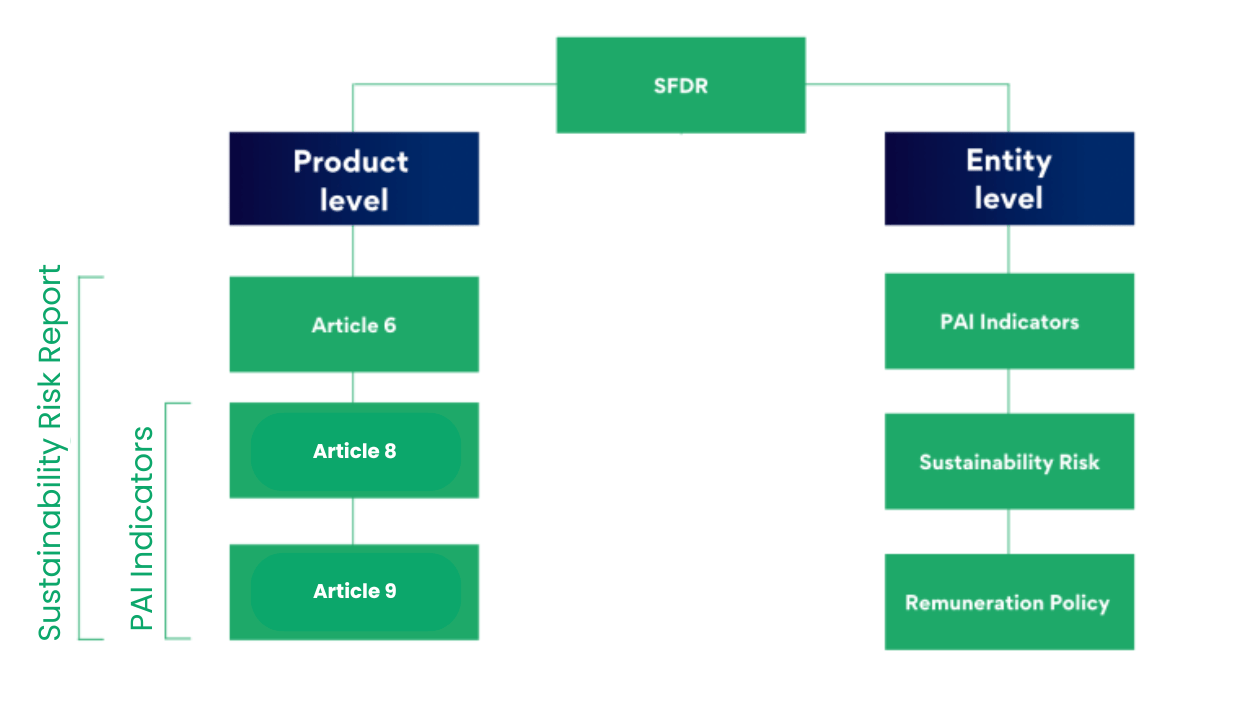

SFDR is a set of EU regulations that require asset managers and other financial market participants to publicly disclose ESG information around their investment decisions and financial products, whether or not they are listed as sustainable.

SFDR reporting aims to create a unified set of ESG reporting standards within the EU, thereby increasing transparency around sustainability-related risk, integration and potential impact of financial products available on the market. It combats greenwashing by creating greater transparency around ESG claims, which in turn helps fund managers and other investors compare and contrast the sustainability information of businesses.

Every financial market participant or financial advisor based in the EU must comply with SFDR reporting, across asset classes and including private equity. Non-EU participants marketing funds or products within the EU must also adhere to SFDR regulations for each fund or product they market to EU-based clients (i.e., fund-level disclosures only). Disclosures are required whether or not funds or products are marketed as ESG-focused.

The following deadlines apply to SFDR’s rollout over the course of four years, from its inception in 2021 until mid-2023:

March 10, 2021 – The first provisions of SFDR came into effect, requiring information at the entity level on whether or not a firm currently complies with the regulation.

January 1, 2022 – The first level of alignment with the EU taxonomy classification framework came into effect, requiring additional climate-related disclosures.

January 1, 2023 – The second level of alignment with the EU taxonomy will come into effect, requiring additional disclosures for environmentally-aligned funds. Disclosing the Principal Adverse Impact (PAI) statement (more on this below) at the entity level begins.

June 30, 2023 – The PAI annual statement is to be reported on June 30 every year.

SFDR disclosure requirements can be divided into organization-level reporting and fund/product-level reporting.

At the organization level, firms must at least disclose:

At the fund/product level, organizations must at least disclose:

SFDR also classifies funds/products into three categories that are subject to their own disclosure rules. They are:

Article 6 Funds: funds that do not integrate sustainability factors into the investment process, and can include investments excluded by ESG funds e.g. tobacco or thermal coal companies

Article 8 Funds: funds that promote and integrate ESG into their investment process

Article 9 Funds: funds that have the objective of sustainable investment

SFDR is a rigorous regulation. Automating SFDR’s indicators would allow businesses to simplify an otherwise complicated, expensive and time-consuming process. Managing sustainability information in the cloud, rather than through manual mechanisms such as spreadsheets, keeps this data accessible, secure and, importantly, easier to analyze and benchmark to inform strategy and future performance. Technology-based solutions such as ESGTree’s entirely customizable ESG data platform allow investors to monitor, analyze, and benchmark portfolio company performance based on the exact indicators and requirements that are critical to them.

As a comprehensive set of ESG rules, SFDR was devised by regulators themselves, as opposed to recommendations from rating agencies, financial institutions or other member-based organizations and market actors. This makes it the first of its kind, and a robust start to the consolidation of ESG standards globally.

While ESG reporting templates are varied, SFDR is a significant step towards the consolidation and harmonization of ESG worldwide. While public markets are the first affected, the push for greater ESG accountability in private markets is already beginning. Now more than ever, all organizations should train their eye towards staying ahead of regulation and benefiting from strong ESG policies.

For more information on the SFDR Reporting Solution, please contact us at :

ESGTree helps private capital investors stay ahead of regulation and easily collect, analyze and report their ESG data by harnessing the power of the cloud.

Our GP users have been rated in the top 10% of ESG performers by their LPs

Our GP users have been rated in the top 10% of ESG performers by their LPs

Canada: ESGTree, CPA 4th Floor, 140 West mount Rd N, Waterloo,

ON N2L 3G6, Canada

United Kingdom: ESGTree, 33 Queen Street, London EC4R 1AP, United Kingdom